The paper summarized here is part of the fall 2024 edition of the Brookings Papers on Economic Activity, the leading conference series and journal in economics for timely, cutting-edge research about real-world policy issues. Research findings are presented in a clear and accessible style to maximize their impact on economic understanding and policymaking. The editors are Brookings Nonresident Senior Fellows Janice Eberly and Jón Steinsson.

See the spring 2024 BPEA event page to watch paper presentations and read summaries of all the papers from this edition. Submit a proposal to present at a future BPEA conference here.

The federal government and its central bank, the Federal Reserve, are legally required to promote maximum, or full, employment but the law doesn’t define what that is and economists haven’t agreed on a definition.

Policymakers at the Federal Reserve, which also is required to promote price stability, often use the NAIRU (non-accelerating inflation rate of unemployment) as a proxy. That’s the lowest unemployment rate consistent with price stability.

But a paper discussed at the Brookings Papers on Economic Activity (BPEA) conference on September 27 argues that “social efficiency” is the most appropriate translation of the legal concept of full employment. And it suggests that the NAIRU doesn’t measure whether the labor market is efficiently matching workers with jobs.

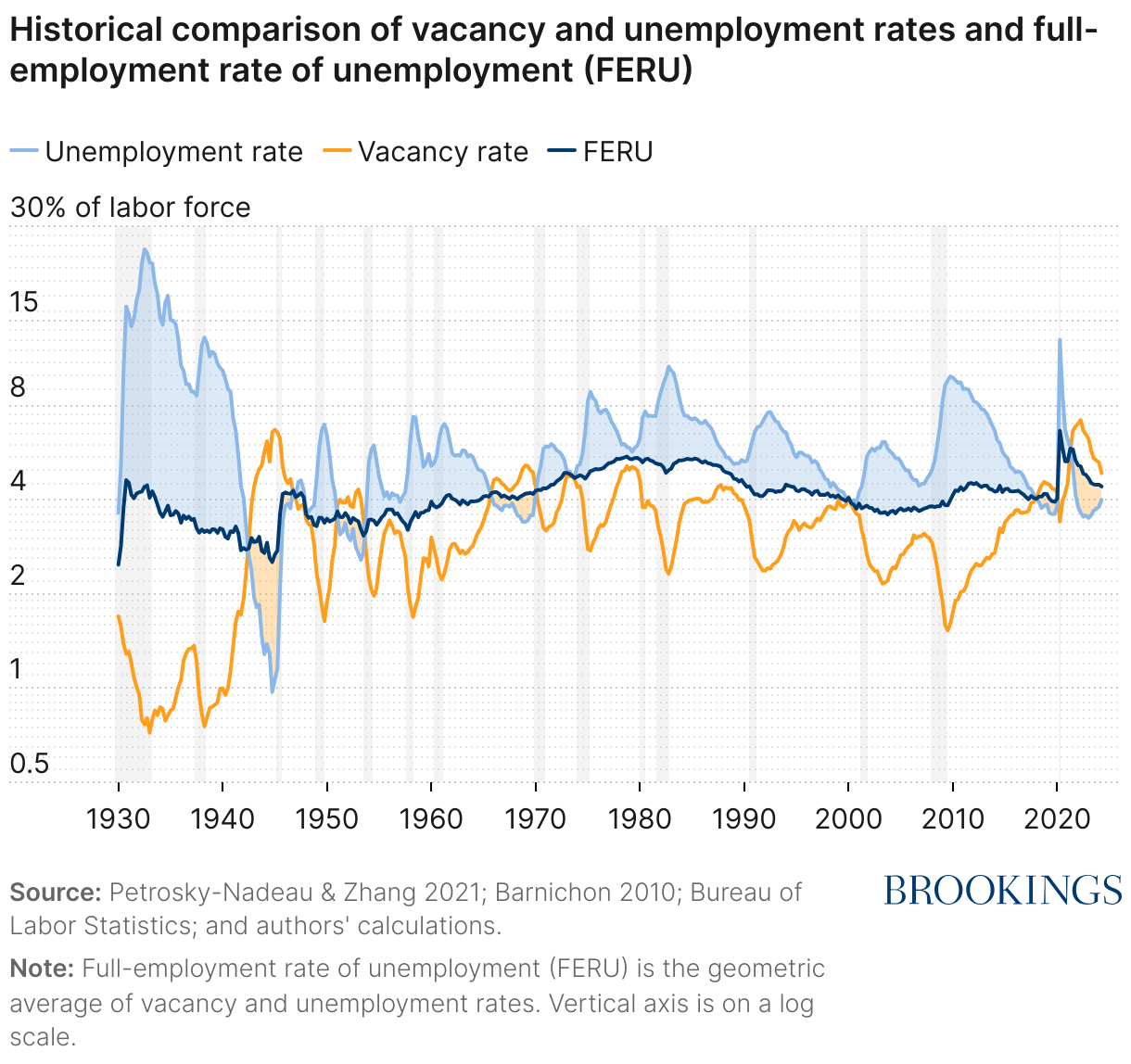

Using efficiency as the criterion, the paper—”u* = √uv: The Full-Employment Rate of Unemployment in the United States”—argues that the best measure of full employment is the midpoint (in log scale) between the unemployment rate (jobless workers as a percentage of the labor force) to the vacancy rate (job openings as a percentage of the labor force).

When vacancies are plentiful, unemployed workers find jobs quickly, but employers spend time and effort on recruitment that could be more productively spent on other activities, the paper argues. Conversely, when vacancies are scarce, unemployed workers are unproductively idle for longer.

“The labor market is efficient when there are as many jobseekers as vacancies…, inefficiently tight when there are more vacancies than jobseekers…, and inefficiently slack when there are more jobseekers than vacancies,” write the authors, Pascal Michaillat of the University of California, Santa Cruz and Emmanuel Saez of the University of California, Berkeley.

They compared the unemployment and vacancy rates from 1930 to 2024. The midpoint (in log scale) between the two—their definition of full employment rate—averaged 4.1%.

Generally, the unemployment rate is higher than the full employment rate—especially during recessions, “meaning that the U.S. labor market has generally been inefficiently slack,” the authors write. “The labor market has only been inefficiently tight during major wars … and around the coronavirus pandemic.”

The unemployment rate was 4.2% in August and the vacancy rate was 4.6%, suggesting the full employment rate of 4.4%, Michaillat said in an interview with The Brookings Institution. “These numbers indicate that the U.S. economy is now almost back to full employment after having been overheated for three years,” he said. The vacancy rate peaked at 7.4% in March 2022 (comparable to the World War II period) and the unemployment rate bottomed out at 3.4% in April 2023, a 54-year low.

Citing a separate paper they wrote this year, the authors suggest that the unemployment rate will soon exceed the vacancy rate and that in August the probability that the United States was in recession was 48%.

“Vacancies have been falling for two years and unemployment has been rising for about a year,” Michaillat said. “Once you cross the threshold, you generally don’t stop there,”

The authors also use their measure of full employment to suggest the Federal Reserve could have moved much sooner to rein in inflation in 2021 and 2022. They calculate that, after the pandemic recession, the labor market reached full employment in the second quarter of 2021 and a year later reached its tightest level since the end of World War II. Meanwhile, 12-month inflation as measured by the Federal Reserve’s preferred price index pushed past the Fed’s 2% target in March 2021 and exceeded 5% by that October. Yet the Fed, which had lowered its target interest rate to near zero to support economic growth during the pandemic, did not start increasing interest rates to curb inflation until March 2022.

“It is unclear why the Fed did not start tightening monetary policy earlier,” the authors write. “One entire year passed between when the labor market became too tight … and when the Fed increased rates.”

Authors

CITATION

Michaillat, Pascal and Emmanuel Saez. 2024. “u* = √uv: The Full-Employment Rate of Unemployment in the United States.” BPEA Conference Draft, Fall.

-

Acknowledgements and disclosures

David Skidmore authored the summary language for this paper. Chris Miller assisted with data visualization.