The paper summarized here is part of the fall 2024 edition of the Brookings Papers on Economic Activity, the leading conference series and journal in economics for timely, cutting-edge research about real-world policy issues. Research findings are presented in a clear and accessible style to maximize their impact on economic understanding and policymaking. The editors are Brookings Nonresident Senior Fellows Janice Eberly and Jón Steinsson.

See the spring 2024 BPEA event page to watch paper presentations and read summaries of all the papers from this edition. Submit a proposal to present at a future BPEA conference here.

Congress and presidents could avoid an explosion of federal debt by returning to an era when they regularly restrained spending and raised taxes in response to projected budget deficit increases, suggests a paper discussed at the Brookings Papers on Economic Activity (BPEA) conference on September 27.

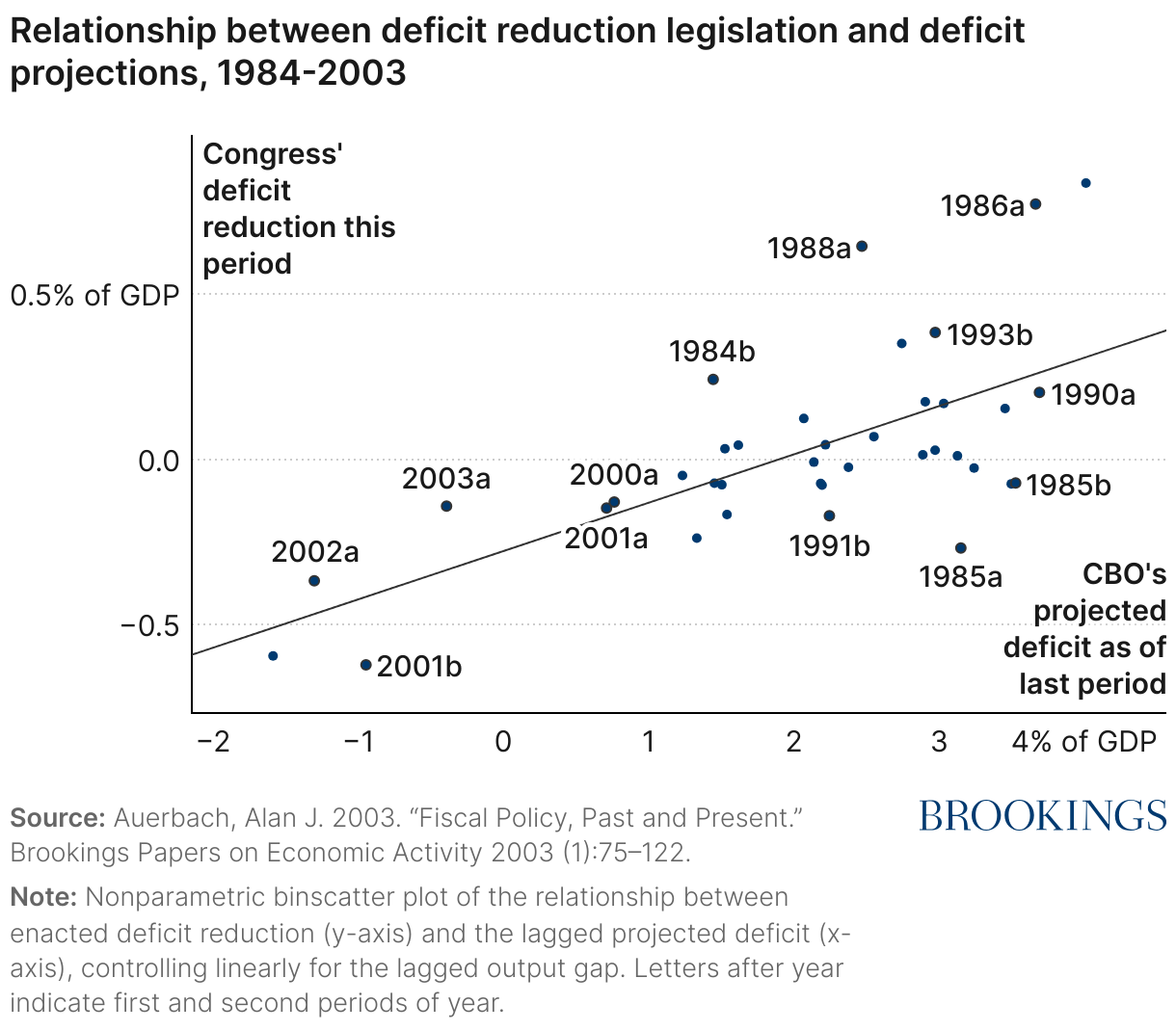

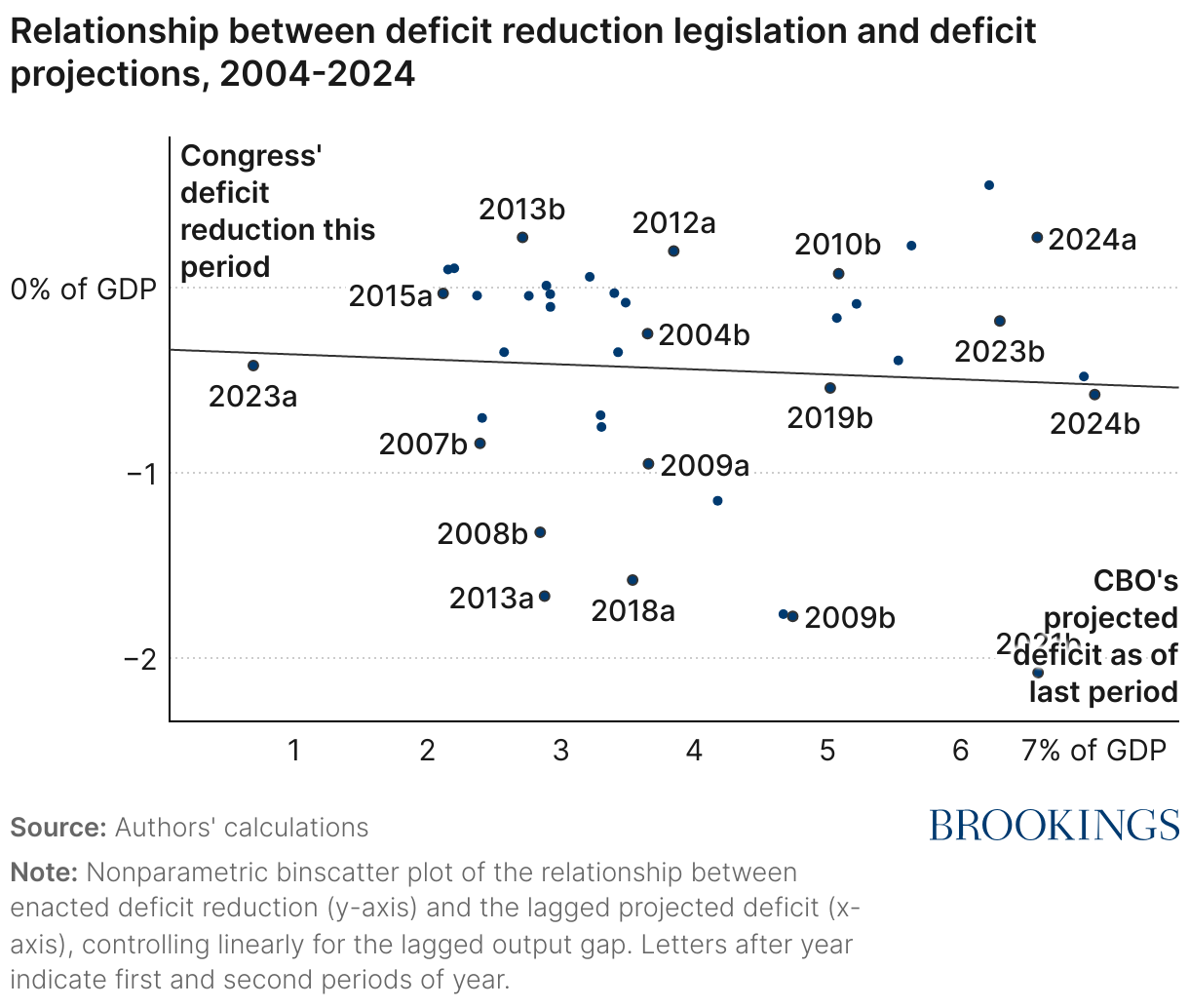

According to the paper—”Robust Fiscal Stabilization”—from 1984 to 2003 Congress reduced the deficit (the annual gap between federal spending and revenue) when projected deficits rose. But, on average, it has not responded to projected deficits from 2004 to 2023.

“Year-to-year feedback has disappeared,” write the authors, Alan J. Auerbach and Danny Yagan of the University of California, Berkeley. They note that federal debt has risen from about a third of U.S. annual economic output (gross domestic product, or GDP) in 2000 to nearly 100% now and is projected to continue increasing.

Relying on an array of empirical evidence drawn from past budget and economic trends, the authors model the fiscal path over the next century. They account for the possibility of economic shocks such as the Great Recession of 2007-2009 and the COVID-19 pandemic, as well as the possibility that interest rates paid on government debt could return to persistently higher levels.

They then examine the fiscal path under several responses to projected rising deficits and government debt, including regular ongoing adjustments such as occurred from 1984 to 2003 and sudden deficit reductions. They find that gradual adjustment over the coming decade would cumulatively reduce the primary deficit (the deficit excluding debt service) between 0.5% and 1.2% of GDP. That would be enough, with 95% probability, to avoid the debt ballooning past 250% of GDP over the next century. In contrast, a wait-and-see strategy of taking action only when it must be taken would require the government to be able to undertake two larger deficit reductions of 1.5% of GDP in a 12-year period, they find.

Fiscal rules such as the Gramm-Rudman-Hollings deficit targets of the mid-1980s, while an expression of Congress’ intent, can be repealed or superseded, the paper notes. What matters is whether, in practice, Congress restrains spending and raises taxes when needed.

“We need to do something about the deficit … and waiting until things get really bad is a major gamble,” Auerbach said in an interview with The Brookings Institution. “We once had government that was responsive to this problem in both Republican and Democratic administrations and we don’t now, in both Republican and Democratic administrations.”

Authors

CITATION

Auerbach, Alan J. and Danny Yagan. 2024. “Robust Fiscal Stabilization.” BPEA Conference Draft, Fall.

-

Acknowledgements and disclosures

David Skidmore authored the summary language for this paper. Chris Miller assisted with data visualization.