Introduction

At the intersection of Grand River Avenue and Evergreen Road in Detroit—in the heart of a resilient, moderate-income, majority-Black community with blocks of stately single-family homes, a historic district, and a vibrant farmers market—a prominent corner parcel of commercial real estate (CRE) sits vacant. In Baltimore, the 1-mile stretch of York Road going north from Loyola University Maryland has three dollar stores. And on the far southeast side of Cleveland, just down the road from the “Dream Town” of Shaker Heights, empty buildings and vacant parcels dot the Lee Road corridor. There is no shortage of entrepreneurs with ideas nor a lack of market demand for retail and services in these communities. But instead of local commerce and local ownership of promising commercial properties, resident economic activity in these largely Black communities leaks elsewhere. Residents have to travel farther to get services and amenities. Both the residential and commercial tax bases languish.

Neighborhoods do not all start from the same line in the race for capital. Research from the Urban Institute has vividly illustrated how unequal capital flows are both across and within cities.

How should stakeholders understand the challenge of revitalizing commercial corridors and fostering inclusive ownership in majority-Black communities where residents are living on low and moderate incomes (LMI)? When financiers, impact investors, or government officials offering tax credits are talking about this challenge, they say that the dollars exist but that they cannot find viable projects that are big enough and ready for investment. However, we have heard and shared the stories of local entrepreneurs who care about these communities and who want to work on the strategic and catalytic small projects that will make a material impact in their communities in terms of retail availability and community ownership. Entrepreneurs who are pursuing these types of projects, which may be smaller in size and/or dollar amount than a typical target of commercial investors, encounter a stack of structural barriers, such as appraisal bias, redlining, and a need for predevelopment capital. It is a chicken-and-egg problem. Commercial corridor revitalization (hatching a baby chick) requires both a pipeline of projects with an articulated investment thesis and local ownership (the egg) as well as patient, flexible financing (the chicken), but you cannot have one without the other. How do relevant stakeholders fix this?

To answer this question, we undertook the Buy Back the Block Lab, engaging with local real estate innovators in Detroit, Baltimore, and Cleveland who are running organizations that are well-positioned to provide communities with solutions and strategies for surmounting these typical mismatches, accessing capital, and fostering local ownership to soundly structured and viable local projects.

There are three intersecting problems creating this chicken-and-egg confusion:

- Potential investors overestimate risk in Black and brown communities and/or are overtly discriminating because of personal bias or structural racism.

- Fixed transaction costs motivate movers of capital to look for larger projects.

- Mainstream finance, legal, and operational players do not yet understand and accept community ownership mechanisms.

The result is a fundamental mismatch between how investors with capital deprioritize small, investment-ready opportunities in majority-Black LMI communities and the stated needs of residents of these places that seek to have an ownership stake in CRE. There are small, viable, momentum-building projects that communities seek to bring to fruition, and what is missing is a way to identify, package, and bundle the financing needed by small transactions and then connect the projects to the capital that is seemingly readily available for only the big projects. To illustrate this, we contrast data from commercial corridors across three majority-Black cities: Detroit, Cleveland, and Baltimore. We then offer practical actions for community-based organizations and entrepreneurs, philanthropists, and policymakers to enable incremental, yet transformative, steps to “buy back the block.”

More on methods: Design of the Buy Back the Block Lab

The goal of this applied research project was to learn more about the barriers to inclusive revitalization and ambitions for shared ownership of CRE in majority-Black neighborhoods. In addition, we endeavored to share reality-based strategies necessary for gaining site control of CRE, completing due diligence, making the case for capital, and ultimately structuring community investment vehicles. We believed that we could overcome hurdles by leveraging the expertise of community leaders on the ground in three cities and working collectively to bring their vision for locally owned CRE to fruition.

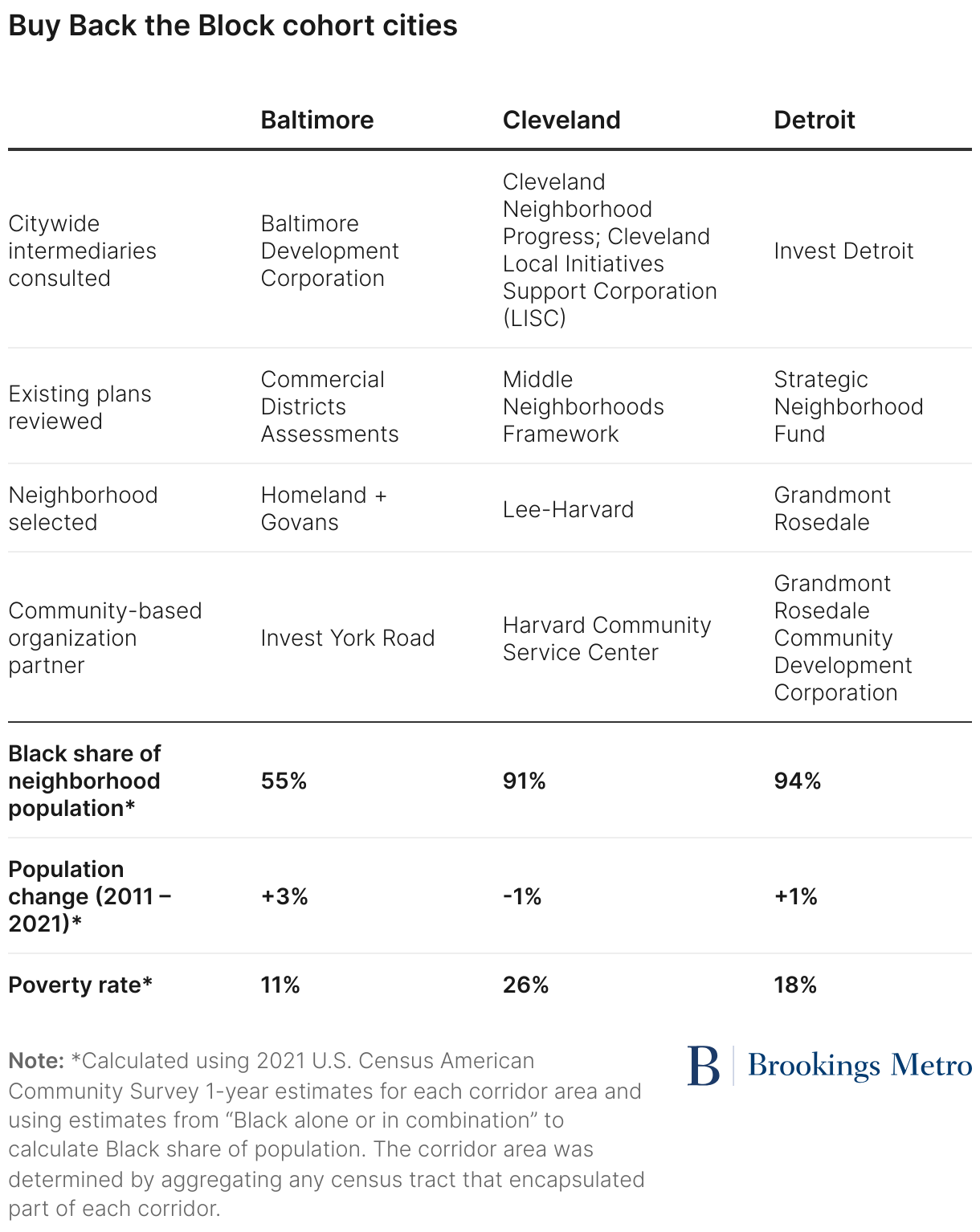

We selected one commercial corridor in each city by visiting each market, consulting with citywide intermediaries who specialize in community and economic development, reviewing existing commercial corridor plans and prioritization frameworks, exploring market and demographic data trends for potential neighborhoods while looking for the right combinations of demographics and location characteristics (majority-Black; stable or growing population; and moderate-plus income households are the majority), and completing a project fit assessment to evaluate interest and capacity with potential community-based organization partners. Our lab participants engaged in a planning process using existing demographic data and neighborhood planning materials to create a vision for how they might work collaboratively across stakeholders in their respective cities to add new research and project implementation capabilities to their plans with support from one another and Brookings as a learning cohort. The process and participants are summarized in Table 1.

The case for locally led investing in neighborhood commercial corridors

Reason 1: Strong neighborhoods need functioning commercial corridors

Commercial corridors create the first impression of a neighborhood. When they suffer high vacancy; are boarded up and blighted; are dominated by extractive or predatory retail such as dollar stores, liquor stores, furniture rental companies, and payday lenders; or are “under-leased” to local tenants with no buildout allowances and unattractive façades, they can become a liability to a neighborhood.

More broadly, as Majora Carter argued in Reclaiming Your Community, investing in and even subsidizing third places offering community services, providing amenities, and spurring entrepreneurship can discourage depopulation of communities of color and especially help retain and attract more middle-income and professional people. Half of low-income white people live in mixed-income neighborhoods, which reduces their exposure to the harmful concentration of poverty. Addressing the needs and desires of moderate-income households of color is part of the solution to the race- and income-segregation that steeply, disproportionately afflicts Black, Hispanic, and Native American people.

Reason 2: Functioning commercial corridors are part of ensuring resilient, sustainable local jurisdictions

Beyond the benefits to neighborhoods and the people who reside in them, there is a collective public interest in fostering neighborhoods that directly offer goods and services and recycle wealth locally. Better-resourced commercial corridors bring in more property taxes, from CRE corridors themselves and from nearby homes, as well as increased sales tax revenue for municipalities for neighborhoods where there is cross-jurisdictional leakage.

There is a robust evidence base that property values across asset classes rise in communities with more retail amenities. In a study of Louisville, Kentucky, published in 2015, a trio of researchers found that having larger and more diverse retail offerings nearby1 had a statistically significant and large positive effect on home values; had a significant and negative relationship with foreclosures over time; and had a negative relationship with crime rates in some cases.

Reason 3: To get great outcomes, a corridor’s tenant mix needs curation

Why is it important for there to be a local voice in commercial corridor development? The existing evidence base points to the conclusion that it takes more than high occupancy to make a strong commercial corridor. In other words, it is not necessarily better to have any tenants than to have no tenants. For example, the Louisville study found the beneficial relationship between retail, homeownership, and crime only in majority-white neighborhoods. However, as we have found in previous research, this may be explained by the fact that conventional retail is underrepresented in majority-Black neighborhoods at all income levels, leading to disproportionate shares of predatory retail, which other research has found is related to crime prevalence. The overall quality of the retail mix matters—but this is measured at the neighborhood level and is a bigger consideration than any one property owner. It is logical, therefore, that there must be some kind of coordination or shared mission among multiple actors in a neighborhood’s CRE submarket to achieve positive neighborhood-level outcomes.

The opportunity: The unacknowledged, unmeasured, likely enormous pipeline of projects in disinvested communities

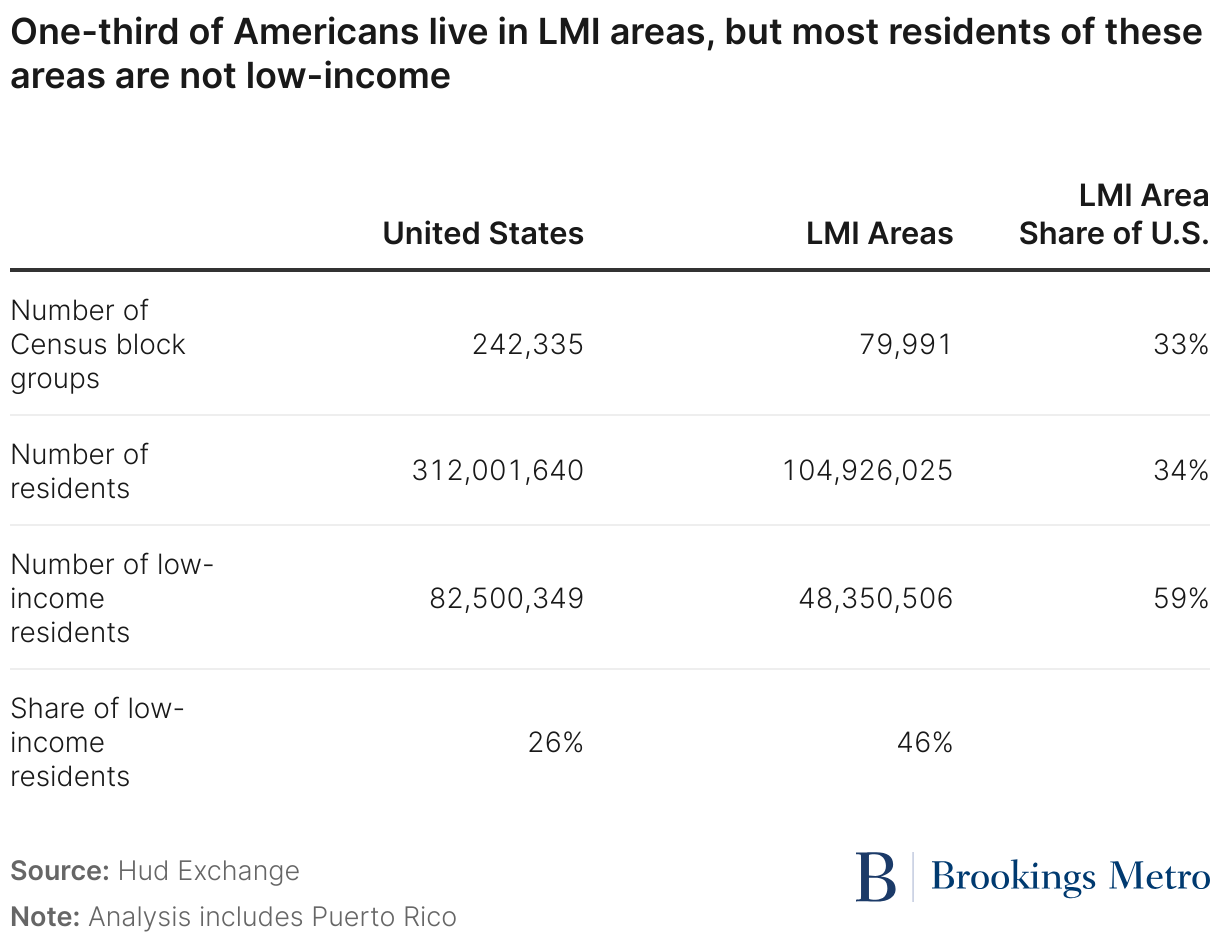

Much of the discourse on economic inequality focuses on the gulf between very rich neighborhoods and very poor neighborhoods. However, there are a lot of Americans living in the middle. For the purposes of administering community development block grants, the U.S. Department of Housing and Urban Development (HUD) defines LMI areas as U.S. Census block groups where at least 51% of residents have either low or moderate incomes relative to the median income in their area. An analysis of the HUD estimates relating to these thresholds is presented in Table 2.

We found that one-third (34%) of all Americans live in LMI areas. However, actual low-income residents (46% of residents) are not a majority in LMI areas. Thus, a modest majority of the people living in these areas have incomes that meet the moderate-income threshold or higher. This basic math suggests that there is untapped wealth in disinvested communities. Instead, investors are not adequately recognizing and placing capital appropriately because of a combination of misperceptions (such as racism, discomfort, a lack of cultural competence/familiarity with these kinds of communities) and systemic barriers (such as redlining or a lack of comps). These numbers illustrate both the vast market size and hidden market strength of LMI areas—the foundation of a business case for increased investment.

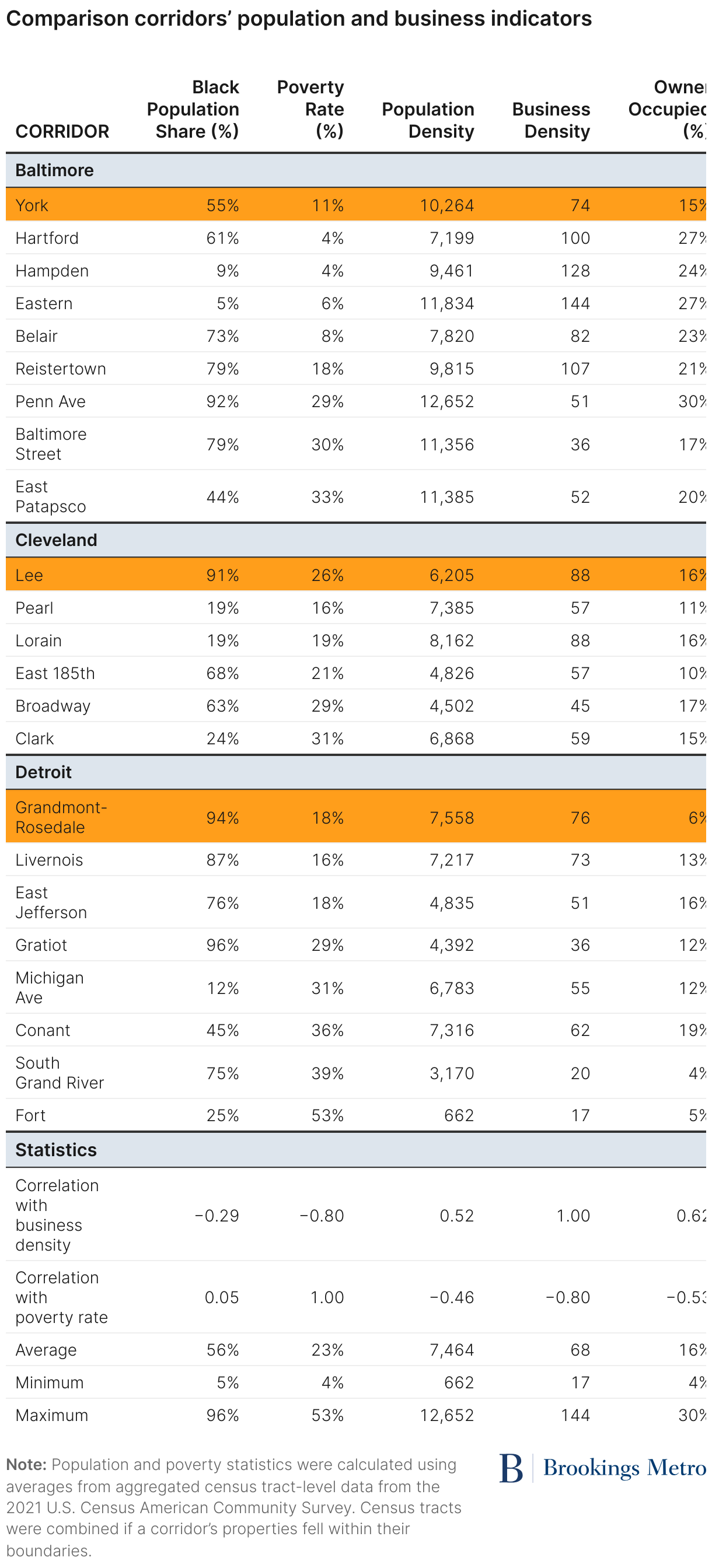

A closer look at the commercial corridors we studied in our applied research project, in contrast with other commercial corridors from the same markets, also helps illustrate the potential pipeline. We assembled a unique dataset of measures of retail market strength and retail activity for 23 commercial corridors across the three cities.2 Retail market strength as a construct is composed of two dimensions that crudely measure consumer demand: wealth within the market and the overall size of the market. We quantify market strength by poverty rate (lower rates of poverty indicate more households with more disposable income) and population density (a measure of market size, which directly speaks to market strength).

We note that there are many options and alternatives for quantifying the constructs composing retail market strength and that conventional measures of market strength can underestimate urban market potential. Similarly, there is no public or private dataset of all retail businesses that is up to date and accurate at a hyperlocal level. To overcome this information gap, we measured retail activity using an approach developed by Theo Goetemann of Basil Labs, a consumer intelligence consultancy, which consists of scraping from Google Maps the existing establishments on a commercial corridor and then normalizing this aggregate count by mileage (corridor length).

These corridors span a variety of neighborhood contexts and are summarized in Table 1. Of the 23 corridors we studied, the most vibrant was a segment of Eastern Avenue in the Highlandtown neighborhood of Baltimore, where we found 144 active businesses per square mile. The most distressed was Fort Street on the border edge of the Southwest neighborhood of Detroit, with only 17 businesses per square mile.

This sample was too small to be analyzed using statistical regression methods. However, we tested for simple bivariate correlations in the dataset to hypothesize explanations for the very large variance in retail activity across these corridors. First, we found that both Black population share and the poverty rate were negatively correlated with businesses per square mile across the sample of commercial corridors. However, within this sample, there was essentially no relationship between Black population share and poverty (the two variables had a correlation coefficient of 0.05). This suggests that, while it is generally true that low-income Black people are spatially concentrated in a way that most low-income white people are not, the general spatial relationship between race and poverty does not apply to these particular corridors as a group. In other words, whatever the reason Black population share is negatively correlated with retail activity on these corridors, it is not because the Black population near these corridors is also mostly low-income. While the reason for this negative correlation is unknown, the hypothesis of often-raised laments about “retailer redlining” from higher-income, majority-Black communities like Prince George’s County, Maryland, and Olympia Fields, Illinois, cannot be ruled out.

Population density, on the other hand, is a measure of market strength that is strongly, positively correlated with retail activity for the sample. These directional relationships, in combination, suggest an overlooked market opportunity in majority-Black neighborhoods where population densities are higher and poverty rates are relatively low. The example of York Road in Baltimore is illustrative. York Road has one of the highest population densities in the sample, a relatively low poverty rate, and a majority of the nearby population is Black. If York Road in Baltimore had as many businesses per square mile as Eastern Avenue, there would be almost twice as many (94% more) occupied storefronts on York Road.3

Or compare York Road with Lorain Avenue in Cleveland. Lorain Avenue has a higher poverty rate and lower population density than York Road, which might logically indicate a weaker market and thus less retail activity. However, Lorain Avenue actually has more retail activity per mile than York Road. Lorain Avenue’s Black population share is also relatively low. If York Road had retail activity parity with Lorain Avenue, it would have 18% more storefronts than it has currently. These comparisons provide just a glimpse into the vast universe of potential CRE projects in majority-Black LMI communities.

The barriers: Why doesn’t more investment flow to commercial corridors in majority-Black neighborhoods?

Disinvested neighborhoods in majority-Black communities face challenges because of a doom loop of devaluation, disinvestment, and displacement. This downward spiral can solidify into a seemingly permanent obstacle to developing a pipeline of projects that are ready for revitalization.

Barrier 1: Devaluation

A generation of research has documented systemic differences in appraised values for property (both residential and retail) across segregated neighborhoods. These differences cannot be fully explained by building characteristics or location characteristics such as proximity to undesirable land uses, crime, or school quality. Rather, there is a systemic devaluation effect that impacts majority-Black neighborhoods because of some combination of bias on the part of appraisers and structural problems with the way the appraisal system works.

As described in greater detail in prior Brookings Metro research, one consequence of devaluation is that Black homeowners tend to be taxed at higher rates than white homeowners. In addition, appraisal (for the purposes of borrowing or selling) and assessment (for the purposes of taxation) are separate professions and processes, though they use overlapping methodologies. Devaluation creates a paradox in which Black-owned homes tend to be overassessed relative to their market value. Ultimately, devaluation has only downsides for property owners in Black neighborhoods, reducing both wealth and access to debt capital using property as collateral. The latter challenge is a direct barrier to capital flows, as low appraisals are a common reason for loan denials that can stymie sales transactions even when there are willing sellers and buyers, reinforcing the “thin market” conditions of weak demand and inadequate comparable sales that further undermine appraisal methodologies and create a self-reinforcing structural problem.

Barrier 2: Deferred maintenance and depreciation

In urban areas, the Black population tends to be concentrated in neighborhoods where the building stock is older. When combined with residents’ systematically lower access to capital because of devaluation and direct discrimination, this reality gradually creates a creeping drought of deferred maintenance. What this pragmatically means today is systematically higher predevelopment and rehabilitation costs, in terms of both time and money, to complete small but impactful projects in urban core communities. This would be a significant barrier even if redlining truly was completely in the past.

An additional systemic challenge that thwarts commercial corridor development in disinvested neighborhoods is that tax policy discourages longtime owners of vacant, abandoned, and deteriorated commercial property from working with economic development leaders and taking aggressive steps to sell properties so that revitalization can be expedited. But the reality is that in many cases these owners are a problem and getting the property to change hands is the first step to revitalization. For example, recent survey research from Chicago found that the top reason for retail vacancy is poor property management by current owners. However, even if the barrier of devaluation can be overcome, there is an additional finance-related challenge that is specific to CRE.

When owners buy and hold property for a long time, every year they can account for carrying costs and deduct some amount from their taxable income through a process called depreciation. However, when an investment property is sold, in addition to owing capital gains taxes on any increase in value between the purchase price and the sale price, any claimed depreciated value from all years since the purchase is recaptured and taxed as well. This results in a potentially enormous capital gains tax obligation that is not reflective of the fact that real estate has legitimate carrying costs that do not exist in other forms of investments such as stocks. Depreciation recapture is a disincentive to sell property, and that disincentive gets larger the longer the investor has held the asset.

Barrier 3: The challenge of infill

In Rust Belt legacy cities, there is typically also a significant amount of vacant land but many individual parcel owners—making land assembly and consolidation difficult. This is a barrier to redevelopment because modern zoning codes often render historic development patterns nonconforming; new construction projects need to assemble bigger lots to comply with modern setback, parking, and other zoning requirements or to enable mixed-use projects that achieve more objectives and can access more diverse sources of capital.

Barrier 4: Absentee ownership?

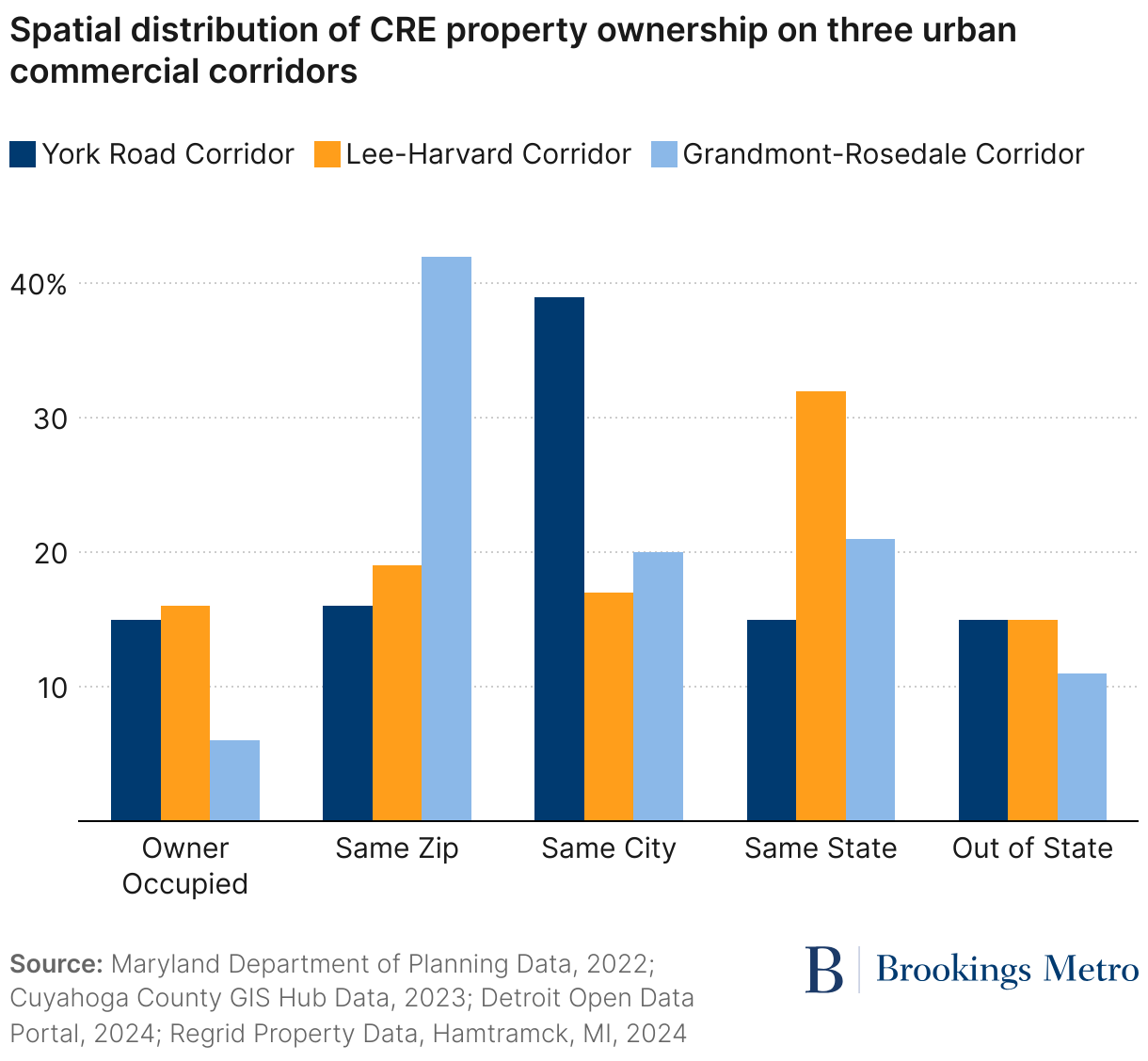

All of these barriers to revitalization have touched on various dimensions of why ownership matters and why ownership must evolve. However, we have also written about the need to localize ownership as an investment thesis, management strategy, and power-sharing mechanism to prevent displacement. To test this hypothesis, we obtained parcel-level local tax records in all three jurisdictions participating in the Buy Back the Block Lab to explore the geographic distribution of CRE owners on the sample of 23 commercial corridors. The results for the three cohort corridors are listed in Figure 1. The very high rate of local ownership in Grandmont-Rosedale confirms the experience of Brian Rice, whose story inspired the Buy Back the Block Lab: simply localizing ownership does not overcome the only barrier to revitalization. However, the low rates of local ownership on Lee Road and York Road highlight that many corridors are held in distant hands, and localizing more ownership can be a logical, if not sufficient, step to revitalization.

In fact, the only category of CRE ownership that was strongly, positively correlated with business density across all 23 commercial corridors was owner-occupancy (with a correlation coefficient of 0.62). Owner-occupancy ranged from 4% to 30% across the 23 corridors, with an average of 16%. This suggests a need to prioritize further research into CRE models that enable conventional and innovative forms of occupant ownership and into policymaking to support such models.

The current state of practice at surmounting these barriers

The cycle of devaluation, disinvestment, and displacement is not at all new. Some of the research cited in this report is decades old. Richard Taub described one generation’s attempt to create new institutions (such as the South Shore Bank) and an organizational ecosystem to break this cycle in Community Capitalism, first published in 1988. From this inspiration, today there is a complex ecosystem of organizations, policies, and programs that has evolved at the federal, state, and local levels to directly respond to this challenge.

In this ecosystem, there are two parallel policies to get debt capital to underserved neighborhoods. On the one hand, in the face of higher costs and perceived risks in communities harmed by past disinvestment, the U.S. policy ecosystem offers the financing mechanism of community development financial institutions (CDFIs) to meet the capital needs of neighborhoods that were overlooked and/or whose lending needs were not properly served by traditional financial institutions. These have been effective at small business lending and housing, but they have a limited track record on CRE. In the 2023 CDFI Survey, only 21% of CDFIs identified CRE lending as either a primary or secondary line of business. To make a difference at scale, America needs alternatives to get capital to real estate projects beyond CDFIs.

Thus, on the other hand, American policy offers the Community Reinvestment Act (CRA), which requires banks to invest in the communities they serve. This is the right general idea, but it has yet to truly unlock the flow of capital to commercial corridor revitalization in disinvested neighborhoods. It remains to be seen if the CRA modernization currently underway will fix this, though new place-based criteria for community development appear to have potential. The ultimate goal should be for banks to get full credit for originating loans and other services that fund or otherwise enable more development of small projects on LMI commercial corridors.

In addition to these policies relating to debt capital, the federal government also offers several substantial tax credit programs to direct equity capital to LMI areas. The two largest tax credits that are relevant for retail real estate are the New Markets Tax Credit (NMTC) Program and Opportunity Zones. These programs have been highly impactful, directing more than $88 billion in equity ($40 billon from the NMTC Program and $48 billion in Opportunity Zones) to LMI communities since 2000. However, the median size of an NMTC project is $3.7 million, similar to the median Opportunity Zone investment of $3.5 million. Yet CoStar reports that the average sale price of a retail property in Baltimore in 2023 was only $1.1 million; in Cleveland only $847,000; and in Detroit only $496,000.4 Like trying to put a jumbo Band-Aid on a paper cut, there is a fundamental mismatch between the treatment and the need.

That said, the Opportunity Zone program was designed to recognize the value of patient capital in real estate revitalization by forgiving a set amount of capital gains invested in targeted LMI areas. And in a sense, the enormous uptake of that program in a very short period of time has demonstrated that there certainly is a pipeline of projects in LMI communities. The problem is that much of the tax benefits and the project pipeline have favored larger investments and larger projects that have no local ownership.

At the local level, many cities have deployed tax increment financing (TIF) to catalyze projects. A recent review estimated that there was over $37 billion in TIF borrowing between 2000 and 2015, putting TIF as a financing source on par with the NMTC Program or Opportunity Zones. However, there are many cautionary notes in the literature on TIFs, such as work from Rachel Weber noting that overuse in Chicago has “contributed to a dangerous oversupply of commercial real estate.” This kind of market distortion is consistent with the fact that TIF districts are creations of legislators, not market demand.

Left still unanswered is the question of what could occupy the enormous middle ground between a fully market-based solution or a policy-based one. The streets in our sample are just a handful of the neighborhood commercial corridors in majority-Black cities and neighborhoods nationwide struggling to access capital to incentivize property development and revitalization. What if there are thousands of projects that are otherwise ready to go and need funding but are not considered big enough to attract a NMTC allocation or for their respective cities to arrange tax increment financing?

A new approach: The next generation of community capital and capacity for CRE

To break the cycle of disinvestment without causing displacement, there is still a need for solutions to overcome project financing obstacles faced by local developers working to jumpstart smaller projects on disinvested, urban commercial corridors.

The current paradigm puts the onus on local communities to assemble their smaller local needs into big projects, which exposes them to tremendous predevelopment costs and risk or otherwise perpetuates disinvestment when they cannot. Both mission-driven and conventional capital increasingly moves only through large transactions. Is this truly because these are the projects that are “transformative,” or is it because their capital sources, whether a conventional loan or a NMTC, have high fixed transaction costs that are incompatible with small deals but generate substantial fees for administrators and lawyers?

The result is that good projects get stuck in the pipeline and never make it to the finish line. Do philanthropic organizations and the public sector accept this because, unless a project is large, it is not changing systems? The real world is evolutionary, not revolutionary, especially for projects that have community buy-in. Flowers in the concrete can lead to bigger things and need just a little bit of watering.

The real capital needed to revitalize commercial corridors in majority-Black neighborhoods is not for what Jane Jacobs called “cataclysmic money” or what an impact investor might call the so-called “missing” pipeline of big visionary projects.5 While big catalytic projects are surely needed and beneficial, for every one of those there are ten smaller projects that could be shovel-ready with much less difficulty—projects with development budgets of $100,000 to $2 million. These projects are the Buy Back the Block targets where there is immediate opportunity for economic development officials, philanthropists, and mission-aligned investors to create local ownership of CRE and foster entrepreneurship in ways that will bring needed goods and services to strengthen LMI neighborhoods.

Some cities have tried to respond to this challenge directly with new economic development programs and strategies. In Detroit, two complementary interventions address this challenge: the city’s Motor City Match program and a city-CDFI collaboration called the Strategic Neighborhood Fund run by Invest Detroit. In Chicago, philanthropic organizations (such as the Chicago Community Trust) have played a consistent role across mayoral administrations in solving this challenge, as have iterations of the Neighborhood Opportunity Fund. These public and philanthropic attempts have responded to capital droughts for CRE by offering grants where the market does not want to make loans. However, this arrangement leaves open the question of whether the most impactful role that philanthropic organizations and the public sector can play is raising the resources to assume a role that could be played by the private sector, or if better regulation or incentives for the private sector could help markets move capital at scale into LMI corridors.

At the federal and/or state levels, a smaller, more incremental application of the same principle as Opportunity Zones could catalyze a substantial number of projects with significant dollar values in urban commercial corridors by unblocking the pipeline through easing the transfer of ownership to local entrepreneurs ready to put real estate to work. The federal government, states with their own capital gains taxes, or localities with high real estate transfer taxes could forgive, say, up to $1 million in basis in LMI areas—a very modest amount in per-project terms in CRE—to structurally facilitate deal flow (the pipeline) in LMI communities.

More money alone is not going to revitalize long-disinvested communities. There is also a need to invest in and develop real estate capacity. Programs like Milwaukee’s ACRE, a cross-sector training and networking certificate program for entrepreneurs of color to enter real estate, are needed in every major market. However, especially for small- and medium-sized cities that cannot build and sustain such programs, and for bigger markets that are just starting out, as part of our lab, we developed a five-module curriculum to introduce the basics of CRE. The curriculum concludes with a discussion of inclusive capital stacks.

Download

It makes sense that communities should have a way to be a part of the next generation of “community capital.” Shared equity models in which local investors can accomplish a mix of political and economic goals make a stronger case for investment—whether that is philanthropic, public, or private investment—in CRE projects. Projects that have raised local capital demonstrate support, literal buy-in, in a materially broader way than any market survey can. In addition, another source of equity thickens the capital stack of a given project, increasing its viability.

There are several legal mechanisms currently available for cultivating shared equity in ways that are compliant with relevant Securities and Exchange Commission guidelines. For example, since 2012, Title III of the Jumpstart Our Business Startups (JOBS) Act has technically allowed anyone over the age of 18 to invest via crowdfunding. And, going all the way back to 1933, Section 3(a)(2) of the Securities Act allows stock offerings exempt from registration and appropriate for nonaccredited investors if secured by a bank’s direct-pay letter of credit that provides investors with liquidity and loss protection (used by the East Portland Community Investment Trust). There are also a variety of other corporate structures that capture the spirit of community ownership and community benefit if not the literal structure of shared equity, such as associations, perpetual purpose trusts, and B corporations.

Invest York Road: Connecting communities

The York Road corridor runs through the center of 24 North Baltimore neighborhoods. With two universities and a major bus route, the corridor is a clear opportunity for investment. However, due to a long history of redlining and unequal investment, it currently serves as a mark of division between Black and white residents. On the west side of the corridor, a majority-white neighborhood has a median household income of over $200,000, while on the east side of the road a majority-Black neighborhood has a median household income of under $60,000. On both sides, the corridor is blighted with predatory retail and disengaged commercial property owners. Invest York Road wants to build community trust by transforming this corridor from a mark of division to a vehicle for community wealth—a “zipper” that brings neighborhoods together. The organization’s vision includes acquiring a vacant property on York Road to potentially host a local business and community gathering space. Property ownership will be financed through a community investment fund that can raise flexible capital and then invest it in one or more real estate projects.

Cleveland Neighborhood Progress: Investing in a working-class Black neighborhood

The Lee-Harvard neighborhood in Southeast Cleveland is a historically Black, working-class neighborhood with rows of occupied single-family homes and the built infrastructure for a thriving commercial corridor through the center. Currently, multiple vacancies and community disengagement have left more to be desired by residents, but a citywide strategy to invest in Southeast Cleveland means new planning capacity and opportunities to convince longtime property holders that change is possible. Cleveland Neighborhood Progress and HCSC envision working together to expand HCSC’s assets and capacity through a shared equity investment deal in which the center invests directly with an existing local property owner who is ready to trust only the right partner. They envision a multipurpose, mixed-use “third space” that will host retail space and a food hall full of companies with local Black owners.

Grandmont-Rosedale Development Corporation: Vibrant Black Main Street

Running through five predominately Black neighborhoods in Northwest Detroit, the Grandmont-Rosedale corridor on Grand River Avenue balances at a tipping point. With a rich history of housing development that was later decimated by vacancy during citywide economic turmoil in 2005 and 2008, the Grandmont-Rosedale corridor is making a strong comeback through the Grandmont-Rosedale Development Corporation (GRDC)’s deep local capacity as well as strategic funding from the City of Detroit, local philanthropic organizations, and community engagement. The corridor is already lined with successful CRE owned by GRDC, including a bookstore, a juice bar, an art gallery, and an upcoming speakeasy. These thriving assets are living proof that localizing ownership can work as an investment thesis. GRDC already has a successful track record as a nonprofit organization taking initial predevelopment risk; raising grant capital; leveraging local expertise to build and renovate properties; and identifying, attracting, and signing tenants to leases. GRDC has accumulated significant equity in the stabilized properties, demonstrating financial viability. Now, the organization can engage the community at a new level: GRDC says that it is investigating offering 49% of the equity interest to local residents. Such an offering has the additional benefit of accelerating commercial corridor improvement because GRDC can use the new liquid equity to start another project while residents enjoy an equity ownership stake in a stable asset that will build wealth and improve community cohesion. GRDC also retains a majority of the equity in the original project to continue building the nonprofit’s own power and sustainability.

Conclusion

We have four recommendations for how government, philanthropic, and nonprofit partners can work together to unlock the next generation of community capital for CRE.

- Redefine what kinds of projects are considered good when evaluating impact and return on investment. If a small project brings new and/or additional needed goods, services, and amenities to a community and performs financially to be sufficiently profitable and self-sustaining, that is good. If such a project is led or owned by a local resident or a person of color (inclusive economic development) and is not extractive (as opposed to businesses offering check cashing or furniture rental at predatory rates) and is not detrimental to residents’ life expectancy, that is even better. If such a project checks all of these boxes and is also desired by residents, that is the Holy Grail.

- Understand that the community development pipeline will never be big enough if it only provides predevelopment capital and grant funds to assist nonprofit developers. The nonprofit lens fosters dependency, and this is not how the rest of the market thinks about projects. The rest of the market is looking for a positive return not just to extract value and get rich but to demonstrate a project’s viability and sustainability. It is therefore strategic to provide grant capital for small projects to for-profit developers and change policy to allow for reductions or deferrals of capital gains taxes to encourage the transfer of long-vacant property in LMI neighborhoods.

- Adopt hyperlocal, place-based economic development strategies and capital flow structures. There is a need for existing economic development organizations and/or strategies derived collectively by local stakeholders to focus on stimulating a cluster of small projects to turn commercial corridors around. (Relevant stakeholders include city- or region-wide intermediaries such as LISC and development authorities as well as community-based organizations such as business improvement districts, Main Streets, and community development corporations.) Such efforts start with working with existing property owners and incentivizing them to reimagine and improve their properties (or sell them so that others can do so). Most municipalities have business and tourism attraction teams that can also be used more intentionally to attract new tenants to commercial corridors. On the capital front, impact investors should support financial vehicles such as predevelopment and community ownership funds that accelerate small projects into pipelines in places over time.

- Embrace new, inclusive deal structures. Real estate professionals and community leaders need ways to collaborate to combine their expertise and capital and to produce more equitable outcomes. There has already been substantial innovation and legislative action to demonstrate and facilitate the viability of multiple new models in localizing ownership of CRE.

There is a difference between transformative investments and transformative projects. If you have $10 million of patient, flexible grant and equity capital targeted to revitalize commercial corridors, instead of thinking of this as one or two projects, what if it was 10 or 20 projects? Many of these projects can be intentionally structured so that local individuals would have an opportunity to invest and participate in the benefits from commercial property ownership.

Authors

-

Acknowledgements and disclosures

The authors thank Andre Perry for reviewing earlier drafts of this work, and Hannah Stephens and Tina Corea for their invaluable research and editorial support. The authors would also like to express gratitude to Rutgers University and the Center for Urban Entrepreneurship and Economic Development at Rutgers Business School for their support. The authors also thank the community partners who engaged with them and shared their motivations, struggles, successes, and innovations. Michael Randall, Edward Carrington, Marsha Bruhn, and Tom Goddeeris from Grandmont-Rosedale Community Development Corporation; Elaine Gohlstin, Richard Goudreau, Thomas Starinsky, Tory Coats, and Briana Perry from Harvard Community Services Center and Cleveland Neighborhood Progress; Stephanie Geller, LaVerne Nicholson-Sykes, Tiffany Preston, Susan Bennett, and Andrew Connor from Invest York Road. This work was supported by the Robert Wood Johnson Foundation, the Kresge Foundation, and the Gund Foundation.

-

Footnotes

- In much of this literature, the independent variable is described as “walkability,” where that construct is measured in large part by the proximity and diversity of the retail mix by Redfin’s “WalkScore.”

- We chose commercial corridors based on analysis of citywide parcel and zoning data. We included every corridor that met the following criteria: they were similar in length to each city’s focus corridor (or we broke them into segments), they were not located in the downtown or city center, and they had a comparable share of parcels zoned for commercial use.

- There are 144 businesses per square mile on Eastern Avenue and 74 businesses per square mile on York Road per Table 3. (144 – 74)/74 = a 94% difference in the concentration of businesses on York Road relative to Eastern Avenue.

- Estimates from www.costar.com, retrieved in March 2024.

- Chapter 16 of Jacobs’ 1961 book The Death and Life of Great American Cities is “Gradual money and cataclysmic money.”